- How to Stay Ahead of Industry Trends

Q3 Decoded: The Seasonal Forces Shaping Revenue This Quarter

4 min read

•

•

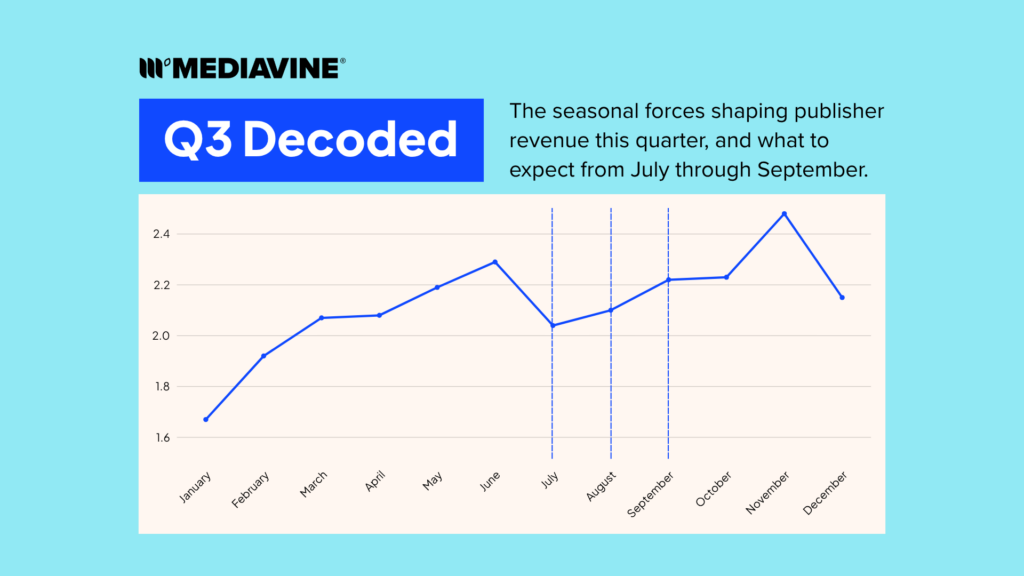

If Q2 felt like a steady climb, Q3 will look a bit different. Rather than building momentum evenly across all three months, the quarter unfolds in two phases: a quieter start followed by a much stronger finish. Looking at July alone won’t tell the full story, Q3’s momentum is expected to build significantly as the quarter progresses.

The forces driving that shift aren’t new. They’re budget planning cycles and end-of-quarter spending behavior, the same ones that have shaped every quarter in this series so far. What’s different in Q3 is a variable the first half of the year didn’t have to deal with: summer.

Here’s what that actually looks like, and how to plan around it.

Early Q3 (July): Budgets Are Fresh, Spending Is Cautious

The first few days of July often carry some residual strength from July 4th spend, then pull back once advertisers return and begin pacing fresh Q3 budgets. That early swing makes July one of the more unpredictable stretches of the quarter, and a poor benchmark for what the rest of Q3 will look like.

The quarterly reset starts after the holiday. By the time advertisers are back from the long weekend, they’ve just come out of Q2’s execution phase, and Q3 budgets are brand new. As always happens at the start of a quarter, spending starts cautiously. Teams are pacing campaigns, testing what’s working, and holding off on aggressive bids until they have more signal.

That means the back half of July is often the softest stretch of the quarter.

Late June and late July are measuring two completely different moments in the advertising cycle. One is end-of-quarter, when budgets are racing to close while the other is the beginning of a new one, when spend is just finding its footing. Comparing the two isn’t an apples-to-apples read on your performance.

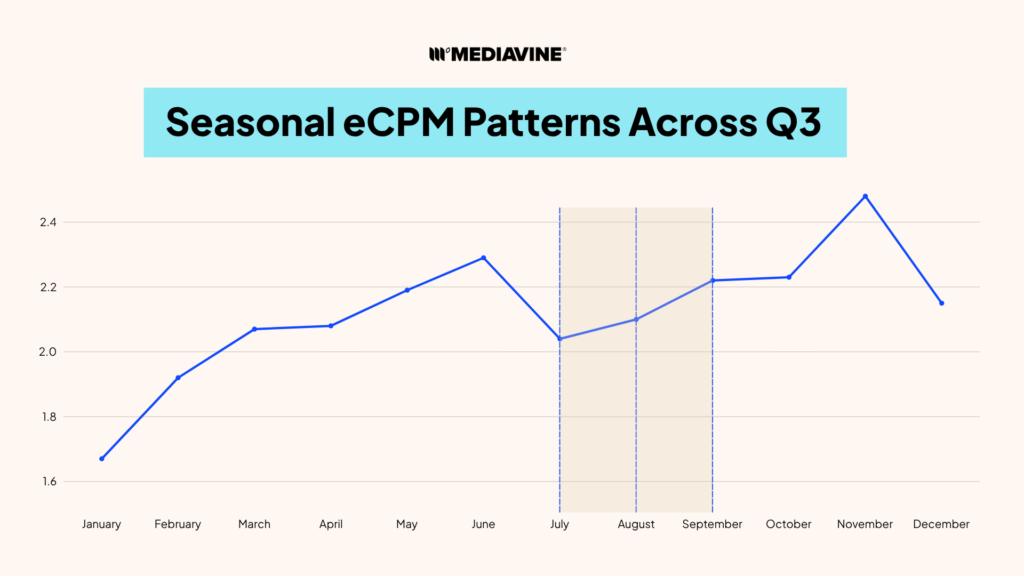

Summer Introduces Real Variability

Q1 and Q2 both follow a fairly predictable rhythm. Q3 doesn’t, and that’s by design, not by accident.

Summer demand behaves differently than the rest of the year because travel picks up, outdoor and lifestyle content sees more attention, and retail moments can inject demand into the market with little warning.

That variability cuts in different directions depending on your niche. A travel or outdoor site might see a real lift in July that a different vertical doesn’t. There’s no single rule that applies evenly across every content category this quarter, which is exactly what makes Q3 harder to predict than Q1 or Q2.

You can’t run the same fixed strategy all quarter and expect it to work equally well in July as it does in September because Q3 requires you to adjust as you go.

Mid-Q3 (August): The Bridge Into Stronger Demand

August is where Q3 starts to turn. Back-to-school campaigns typically begin ramping in late July and build through August, and that spend has real momentum behind it. Unlike the cautious, wait-and-see budgets driving early July, back-to-school budgets come with a hard deadline: the school year starts whether a campaign is ready or not.

That urgency shows up in demand. For publishers in family, education, retail, and lifestyle-adjacent niches especially, August tends to outperform July, and it sets the stage for the stronger push still to come in September.

Even outside those niches, August is worth watching. It’s the bridge between July’s quiet start and September’s close, and it’s usually the first clear signal of which direction the rest of the quarter is heading.

Political Ad Spend Is a Second Demand Driver

Back-to-school isn’t the only added force pushing demand higher this quarter. Midterm election spending adds a second, and unlike back-to-school, it doesn’t wrap up when the school year starts.

Political ad spend is absorbing a growing share of linear and CTV inventory. Advertisers who can’t reach their audiences efficiently through those channels are moving budget into display and online video instead. That pressure builds through August and September and peaks in October, meaning it carries this lift past Q3 and into the start of Q4.

For publishers, that’s demand shifting in your favor. More competition for the same display and video inventory usually means better rates, though the timelines are tighter and buying behavior looks less predictable than a typical cycle.

End-of-Quarter Budgets Drive the September Push

Two forces are now stacked on top of each other heading into September. Election-driven demand is still building and the same end-of-quarter budget mechanic that made late June the strongest part of Q2. As Q3 winds down, unused budget becomes a problem advertisers actively want to solve. Spending accelerates in the final weeks of the quarter as teams push to use what they’ve allocated before it’s gone.

That means late September tends to meaningfully outperform late July.

If you’re comparing performance across the quarter, measure against the pattern. A slow start and a strong close are actually the same story, just at different points in the three-month arc.

How Publishers Can Stay Ahead of Q3 Trends

A few practical ways to work with this pattern instead of reacting to it:

- Hold your best summer content strategically. If you have strong travel, outdoor, or seasonal lifestyle content, plan for it to carry weight through the whole quarter, not just the first few weeks.

- Set realistic expectations for late July. A soft stretch after the July 4th bump is normal, not a warning sign.

- Watch for the back-to-school ramp in August. If your content touches family, education, or retail, this is often the first real sign of momentum building toward September.

- Watch for one-off demand spikes. Major retail or platform events can move the market on short notice, on top of the broader seasonal pattern.

- Keep late-September performance in perspective. It’s typically the strongest stretch of the quarter, not an outlier.

Q3 in the Context of the Advertising Year

Every quarter plays a different role in the annual cycle:

- Q1 resets budgets and strategies

- Q2 stabilizes the market and builds momentum

- Q3 introduces more variability around summer demand, building through August before the strongest activity concentrates late in the quarter

- Q4 delivers peak competition

The calendar changes every year. The behavior behind it largely doesn’t.

If you’re curious about the mechanics behind all of this, our guide on why eCPMs rise and fall throughout the year breaks down the underlying framework in more detail, and our look at the Q2 pattern covers what happens right before Q3 begins.

And if you’re evaluating whether your current ad setup is capturing this seasonal lift the way it should, Q3 is also the ideal window to make a change before Q4 arrives.

Frequently Asked Questions

Why does July feel slower than June? The very start of July often holds up thanks to July 4th spend, but the slowdown sets in once advertisers are back from the holiday and working with fresh, cautiously-paced Q3 budgets. This is the same pattern that shows up at the start of every quarter, not a sign of a problem with your site.

Is a Q3 dip normal? Yes. A softer late July is consistent with the seasonal pattern publishers see every year. What matters more than any single week is how performance trends across the full quarter.

Does August perform better than July? For many publishers, yes. Back-to-school campaigns typically start ramping in late July and build through August, giving demand a real lift ahead of the September push. Publishers in family, education, and retail-adjacent niches tend to see this most clearly.

When in Q3 should I expect the strongest performance? Late September typically outperforms the rest of the quarter, driven by advertisers spending down unused budget before the quarter closes.

Note: This piece follows the seasonality series’ standard disclaimer. Past performance can’t guarantee future results, and broader economic or market conditions can shift the pattern’s timing or intensity in a given year.

About the author

Share this page

The Mediavine Difference

You build content that defines industries.

We build the monetization that powers it.